|

In fact, some policies that strike a chord with the public at present may not be feasible in the long run. Politicians in favor of these policies may not truly believe in them, either, but they know that the smartest political approach is to support these policies until they prove to be invalid. Then they will discard them to embrace more sensible policies. This strategy is highly workable because no one is held personally accountable for the "public opinion," which is changeable in nature and easily forgotten. With this in mind, people may wonder how many of the policies Obama and McCain are now advocating will eventually be abandoned.

In the era of globalization, international cooperation is required to solve the global financial crisis. Unfortunately, there are no established rules for coordinating the economic policies of different countries. Coordination between countries hinges on their willingness to cooperate and their say in international affairs.

Since World War II, the United States has imposed "stabilization programs" featuring liberalization and fiscal stringency on crisis-ridden countries through the International Monetary Fund (IMF). These programs do not help address self-fulfilling crises originating in the financial sector at all. Instead, they often result in plummeting domestic demand and a worsening credit environment that aggravate the crisis. The Russian financial crisis in 1998 highlighted the shortcomings of the IMF's stabilization programs. "IMF recession" and "IMF turmoil" are commonplace in countries that accept the organization's assistance.

U.S. backing is the prime reason the stabilization program has become an IMF mainstay. America's demand that developing countries maintain balanced budgets and give priority to private investment is an ironic contrast to its own efforts to increase public spending and seek fiscal expansion in the 19th century. The ongoing rescue efforts of the U.S. Government apparently run counter to the stabilization program, too. Unlike other countries, the United States, the only superpower in the world, is able to transfer its own crisis, or at least the costs of addressing it, to other parts of the world.

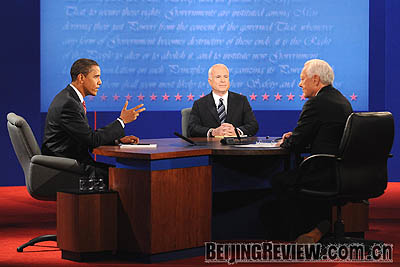

WHO HAS A BETTER SOLUTION? Democratic presidential candidate Barack Obama (left) and his Republican rival John McCain (center) at their last debate at Hofstra University, New York State, on October 15 (XINHUA/AFP)

WHO HAS A BETTER SOLUTION? Democratic presidential candidate Barack Obama (left) and his Republican rival John McCain (center) at their last debate at Hofstra University, New York State, on October 15 (XINHUA/AFP)

John McCain

- Voted for the $700 billion bailout

- His economic proposals include establishing the Mortgage and Financial Institutions trust, an "early intervention program" designed to identify weak financial institutions before they fail; enacting reforms to improve transparency at financial firms; standardizing regulations; and consolidating federal regulatory agencies.

- He would maintain the top tax rate at 35 percent, maintain current tax rates on dividends and capital gains, and cut the corporate tax rate from 35 percent to 25 percent.

- His American Homeownership Resurgence Plan would purchase failing mortgages from homeowners and mortgage providers and replace them with fixed-rate mortgages, at a cost of $300 billion, to help homeowners avoid foreclosure.

- McCain says Obama's tax increases would hinder economic growth.

Barack Obama

- Voted for the $700 billion bailout

- His economic proposals include tax credits for companies that create jobs, a 90-day moratorium on foreclosures, allowing workers to withdraw up to 15 percent from their retirement accounts without tax penalties, and a federal fund that would lend money to state and city governments with shrinking tax revenue.

- He would raise taxes for individuals making more than $200,000 a year, cut taxes for low- and middle-income taxpayers, and eliminate the capital gains tax for small businesses.

- He introduced the STOP FRAUD Act to fight mortgage fraud.

- Obama says McCain's past support for deregulation contributed to the financial crisis.

|