|

|

ALL CLEAR: The National Debt Clock in New York City shows the increasing U.S. debt on August 1 (XINHUA/AFP) |

Since the existing international monetary system is a dollar-standard one, and the dollar bond market is the world's biggest bond market, if a default happened, it would be destructive for the global financial market. The dollar-standard international monetary system would be on the brink of collapse and the U.S. economy itself would take a massive hit. This might also arouse huge political turmoil in the United States, because the biggest holders of U.S. bonds are Americans, not overseas holders. From the boiling reactions of various countries and the worldwide stock market slump in early August, we can see how the debate of debt ceiling in the United States is damaging global market participants' confidence toward the U.S. economy.

An unsustainable trend

It's only natural that the confidence of market participants toward the United States has been undermined, because this country tends to put national benefits before international public benefits and party politics before national benefits. Standard & Poor's downgrading of the United States' credit rating is "not so much because they doubt our ability to pay our debt," but because the rating agency "doubted our political system's ability to act," U.S. President Barack Obama said.

The compromise reached is only temporary relief rather than a solution to the U.S. fiscal predicament. Consequently, the U.S. economy and the world economy will face severe uncertainties in the long term. There is a bipartisan agreement on the 10-year goal of curbing fiscal spending and raising the debt ceiling, but the United States' fiscal deficit and national debt dilemmas have not been removed, but are only deepened.

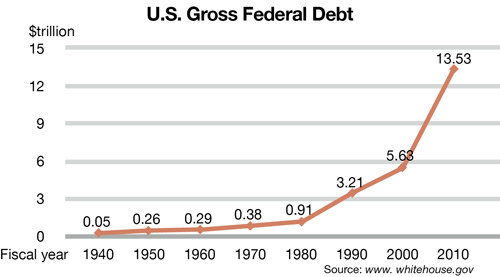

As for the scale of national debt, an absolutely balanced budget is not an ideal choice, since national debt of an appropriate scale has been a necessary tool for modern governments and central banks to carry out macro-control and open market operations. Moreover, as the economy grows, the scale of national debt will rise accordingly. However, if the growth rate of national debt far outpaces economic growth over a long term, a solvency crisis will be unavoidable.

Despite mounting risks, the United States may not be able to effectively restrain the dangerous trend. In short and medium terms, reductions of fiscal spending will lead to the stagnation or even deterioration of the fragile economic recovery in the United States. An analysis in the October 2010 edition of the International Monetary Fund's World Economic Outlook showed fiscal consolidation often curbs economic growth in the short term. "A fiscal consolidation equal to 1 percent of GDP typically reduces GDP by about 0.5 percent within two years and raises the unemployment rate by about 0.3 percentage points. Domestic demand—consumption and investment—falls by about 1 percent," the report said.

If Obama drastically cuts government spending immediately, he would have to suffer the throes of fiscal consolidation in slowing economic growth before the 2012 presidential election. As a result, he may lose the presidency, leaving his successor reaping the fruit of economic growth resulting from an improved financial condition.

In the long run, the U.S. Government will need to control its fiscal expenditures. But can the 10-year goal of cutting government spending stated in the bipartisan agreement be realized? History has told us repeatedly that in the election-oriented United States, we should not excessively expect such a goal to come to fruition. Moreover, most of the government spending cuts are in military items, while military expenditure is just what the Republicans are doing their utmost to maintain.

With confidence toward the United States shaken, market participants will seek new reliable powers to drive the world economy. During the process of seeking alternative economic powers, the overall national strength of the substitutes will be greatly improved. Unlike Western countries with poor economic performance in the wake of the sub-prime mortgage crisis, emerging and developing economies have achieved fast growth in recent years and their proportions in the world economy have increased markedly.

Figures from the April 2011 edition of the World Economic Outlook showed emerging and developing economies accounted for 47.7 percent of the world's GDP in 2010. China alone took up 13.6 percent, close to the proportion of 14.6 percent by the whole euro zone. Growth of emerging and developing economies continues to be far ahead of developed countries and regions.

In terms of indicators in the real economy such as industrial output value, output volumes of many important products and exports of goods, China has already surpassed the United States and ranked first in the world. Even in the financial sector, China has surpassed the United States in terms of some major indicators. For example, the financing scale of the A-share market on the Chinese mainland has been the world's No.1 for several years. When it comes to fiscal conditions, China is also the best among big economies. Under such circumstances, it is natural that people are expecting China's performance amid concerns of a "double dip" of the world economy.

In fact, World Bank President Robert Zoellick said at the organization's 2010 annual meeting that the global economic crisis is contributing to shifts in power relations in the world that will impact currency markets, monetary policies, trade relations and the role of developing countries.

The author is an associate research fellow with the Chinese Academy of International Trade and Economic Cooperation

|