| OPINION

Moderate Yuan Depreciation--More Good Than Harm

As the quantitative easing policy is gradually withdrawn by the U.S. Federal Reserve on the basis of economic recovery, the U.S. dollar will enter a phase of continuous interest rate increases. U.S. dollar's appreciation will become an inevitable trend. Against this backdrop, the Chinese currency, the yuan, will face more depreciation pressure. As a matter of fact, the timing for the yuan to moderately depreciate has come, judging from both external and internal factors. Moderate depreciation of the Chinese currency is not only beneficial for economic recovery, but will also lift China's A-share market.

External factors will inevitably create a weaker yuan. Right now, the U.S. economy is taking the lead in the sluggish global economy. While the dollar is bound to appreciate after interest rate increases, the eurozone and Japan continue to implement their monetary easing policies, which will lead to weaker euro and yen.

The International Monetary Fund (IMF) warned on July 23 that a further rise in the U.S. dollar as a result of the widening monetary policy gap between the United States and other major economies could have a significant negative impact on other countries. In its annual spillovers report, the IMF said lower oil prices, more monetary stimulus in the eurozone and Japan and expectations for interest rate rises in the United States and Britain have created a "spillover-rich" environment. The depreciation of non-dollar currencies will cause global capital to flow out of emerging markets and into the U.S. market, leaving the yuan with depreciation pressure.

Domestic factors also stand in the way of a stronger yuan. An increase of productivity and strong economic rebound has yet to come in China. A country's exchange rate is ultimately determined by its productivity. With rising labor costs, the growth rate of salary is higher than that of the GDP in China, which actually leads to declining productivity in the country. In theory, the government-backed entrepreneurship and innovation campaign will increase China's productivity, but the campaign has yet to bear substantive fruit.

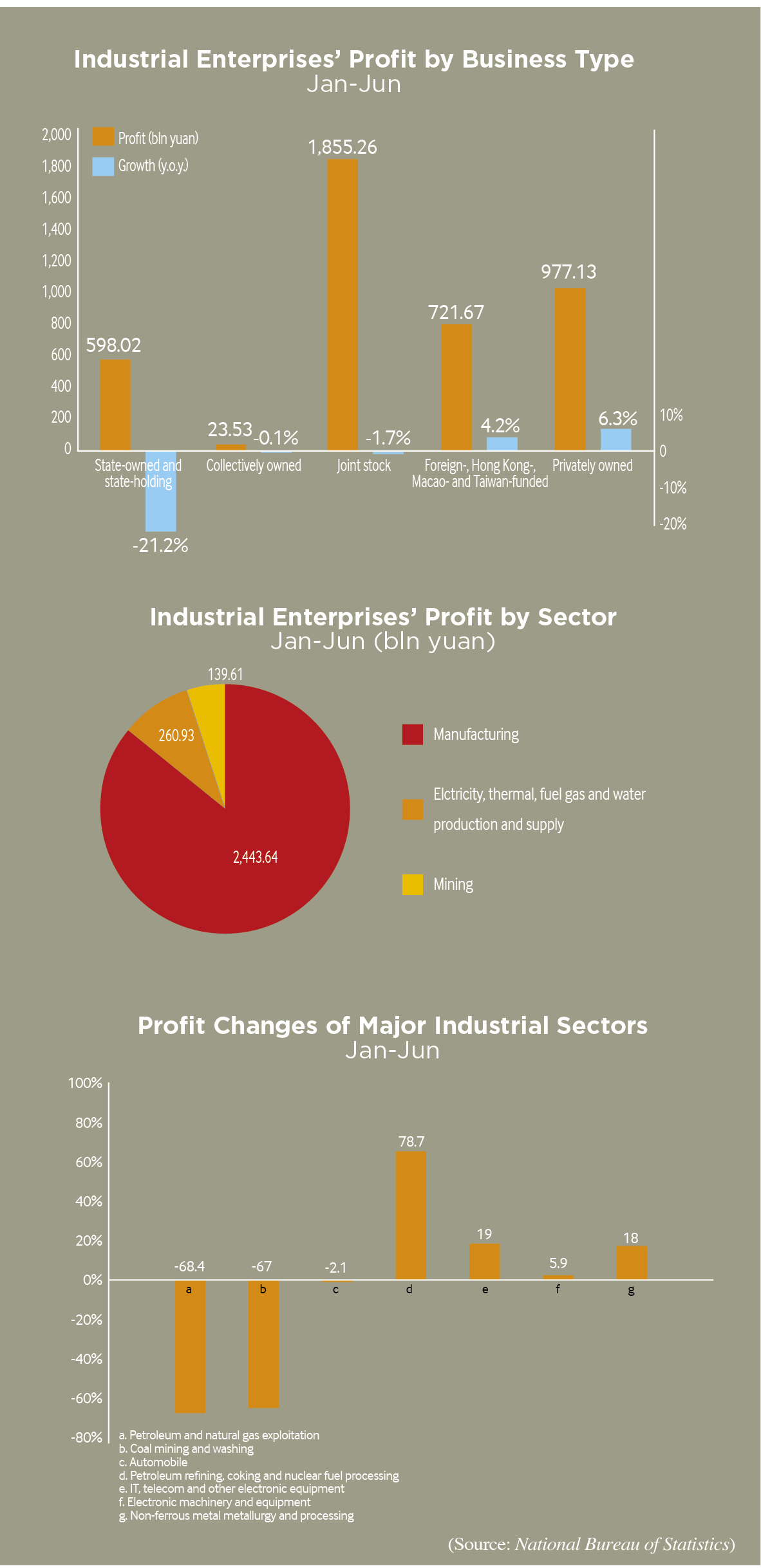

Although Chinese GDP grew 7 percent in the first half of the year, overcapacity hasn't been completely solved. In the first half, profits of industrial enterprises above the designated size--a principal business revenue of more than 20 million yuan ($3.15 million)--amounted to 2.84 trillion yuan ($458 billion), down 0.7 percent year on year. Since the beginning of the year, the Chinese Government has put forward several development strategies--including the Internet Plus, Industry 4.0 and Finance Plus--in an effort to boost economic growth, but they have yet to become real growth drivers.

It takes time for the country to adjust its economic structure and cultivate new growth points, and pains that come with economic transformation are unavoidable. To maintain stable growth, China's central bank lowered its interest rates and reserve requirement ratios (RRR) several times since last year, which is unlikely for the yuan to maintain its strength.

A moderate depreciation of the yuan is needed to boost China's foreign trade, which is mired in difficulties due to weak external and domestic demand. Trade growth failed to meet its target for three years in a row from 2012 to 2014. In the first six months of the year, China's foreign trade totaled 11.53 trillion yuan ($1.86 trillion), down 6.9 percent year on year, with exports increasing 0.9 percent and imports decreasing 15.5 percent. During the period, bilateral trade with the eurozone and Japan decreased 6.8 percent and 10.6 percent, respectively, indicating substantive difficulties faced by the country's exporters. The difficulties are caused by both weak external demand and sustained yuan appreciation that caused Chinese exports to lose their low-price advantage.

By virtue of the above-mentioned factors, the yuan faces an increasing amount of depreciation pressure. Then, is it a good or a bad thing for the currency to depreciate? In my opinion, moderate depreciation of the yuan will help lift the domestic economy; therefore, the advantages outweigh the disadvantages.

Domestically, insufficient demand, shrinking new orders and rising labor costs have restricted economic rebound, and a loose monetary policy is needed to spur growth. Interest rate cuts and RRR cuts by the central bank are targeted at injecting liquidity to the market and lower financing costs for businesses amid economic slowdown. With sufficient liquidity in the domestic market, it's unlikely for the yuan to remain strong against other currencies. On the other hand, moderate depreciation of the yuan can help lower the prices of Chinese exports. The yuan has appreciated 12 percent since July 2014, in conjunction with declining foreign trade in China.

In addition, a depreciating yuan and declining interest rates will make bank deposits less attractive and equities investment more attractive. A sharp housing price rebound is unlikely to be staged in China, as the market is still destocking its large inventory. Therefore, the housing market is not preferred by investors, while the stock market will become a favorable investment object for many people. Although the stock price slump from mid-June to the beginning of July startled many investors, a recent market stabilization following government-backed intervention will attract more investors. Inflow of new capital will help invigorate the vulnerable stock market.

Having peaked after several years of bullish run, the U.S. stock market is likely to enter a stage of market adjustment, especially after the Fed tightens the monetary policy. With a sluggish global stock market, if China's A-share market can continue its bullish trend, global capital will flow into the market, which is good for the internationalization of the A-share market as well as the yuan.

Without any doubt, moderate depreciation of the yuan will inject vigor into the stock market and help sustain a bullish run.

The question is how much depreciation is moderate? In my opinion, if the yuan depreciates against the U.S. dollar while remaining a stable exchange rate against major non-dollar currencies, such as the euro, the pound and the yen, the depreciation should be considered moderate.

This is an edited excerpt of an article by Wu Zhigang, a financial commentator, published in Securities Times

NUMBERS

643 bln yuan

Profits reaped by centrally administered state-owned enterprises in the first half of 2015

800 mln yuan

Microloans extended by WeBank, an online lender set up by Chinese Internet giant Tencent, since its first lending product was unveiled in May

48.63 bln yuan

Money Chinese small and micro firms saved with the help of preferential tax policies in the first half of the year

35%

Proportion of Argentina's meat exports headed to China in the first half of 2015

16%

Year-on-year growth of electricity generated from non-fossil energy in the first half of 2015, which accounted for 22.9 percent of all electricity generated during the same period

5.94 tln yuan

China's tax revenue in the first half of the year, a year-on-year increase of 6.3 percent

138.9 bln yuan

The predicted size of China's online to offline catering industry in 2015

6,223 units

Sales of electric cars in the first half of the year by Beijing Automotive Industry Group Co. Ltd., which had a 66-percent of the electric vehicle market in Beijing

Copyedited by Kylee McIntyre

Comments to yushujun@bjreview.com

|