|

|

(CFP) |

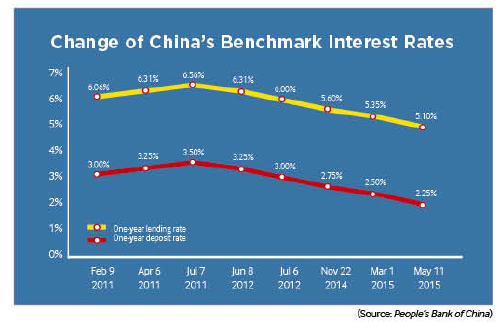

Amid market expectations, the People's Bank of China, the country's central bank, slashed the benchmark deposit and loan interest rates by 0.25 percentage points on May 11.

The event marked the third rate cut in six months. Last November, the central bank announced the first interest rate cut in more than two years, lowering the benchmark rate for one-year deposits by 0.25 percentage points and the one-year lending rate by 0.4 percentage points on November 22, 2014. On March 1, the central bank again slashed benchmark deposit and loan interest rates by 0.25 percentage points.

The rate cut aims at lowering funding costs to facilitate healthy development of the real economy and ensure a modest monetary environment amid the ongoing strategy of national economic restructuring, said the central bank in a statement after the rate cut.

While economic reform accelerates, China still faces economic downward pressure as external demand continues to fluctuate, the central bank said. The country's GDP expanded 7 percent in the first quarter of 2015, the lowest quarterly growth since the global financial crisis.

Prior to the latest rate cut, the central bank also lowered the reserve requirement ratio (RRR) in February and again in April to ease the financing burden on businesses and bolster the economy.

China's low inflationary rate and high level of real interest rates provide ample room to adopt such tools, the central bank said. The consumer price index (CPI), a main gauge of inflation, grew 1.5 percent year on year in April, according to the National Bureau of Statistics. The index slightly rebounded from 1.4 percent in March and February and 0.8 percent in January, the lowest level in more than five years. Meanwhile, even after three rounds of cuts, the one-year deposit rate stands at 2.25 percent, and the one-year lending rate at 5.1 percent.

The cut responds to the economic circumstance and will serve as a boon to lowering financing costs, said Qu Hongbin, chief economist for China at HSBC, who maintained it was a wise move.

The central bank also adjusted the upper limit of the floating band of deposit rates to 1.5 times the benchmark from the previous 1.3 times, marking further steps in an effort to liberalize the interest rate mechanism.

A meeting of the Political Bureau of the Central Committee of the Communist Party of China held on April 30 highlighted the attention it will pay to the economic downward pressure.

The statement released after the meeting said China needs to stick to both the proactive fiscal policy featuring increased public spending, further tax cuts and the prudent monetary policy focusing on guiding monetary flow to the real economy. While emphasizing the key role of investment, the statement also said China should increase efforts to tap consumption potential to foster a new growth impetus.

The central bank made clear that it would continue to implement prudent monetary policy and make moderate adjustments based on changes in liquidity, inflation and economic situation, striking a policy balance between economic restructuring and growth.

No necessity for QE

Despite three cuts in six months, most scholars think it is too early to say whether Chinese QE will come, and easing the monetary policy does not mean the central bank will turn on the liquidity tap.

Commenting on hearsay that China's central bank will adopt measures of quantitative easing (QE) and input base money by purchasing local government bonds, Ma Jun, chief economist of the central bank's research bureau, said it is not necessary for the central bank to input base money by directly buying newly issued local government bonds, and the law also prohibits the central bank from directly offering financing to local governments.

Ma said with targeted re-lending, interest rate and RRR adjustments, and various tools of liquidity control, the central bank is capable enough of maintaining a reasonable level of liquidity as well as stable growth of money and credit.

Chen said previous RRR cuts were made in an accommodative monetary environment. At present, major world economies are using QE measures, so China must reduce the RRR appropriately to adapt to an easy international monetary environment.

Wen Bin, chief analyst at China Minsheng Bank, said the Chinese economy is not yet so bad that the central bank needs to directly purchase local government bonds, a practice prohibited by law, since it has many other measures to release liquidity.

"Currently, China's one-year benchmark lending rate is now as high as 5.35 percent. This means there is still plenty of room for regular monetary policy tools," said Chen Daofu, head of general research office of Research Institute of Finance at the Development Research Center of the State Council.

Reform and solutions

Ma said that besides monetary policy tools, the government needs fiscal policy tools and structural reform to cope with the economic downward pressure.

The Chinese Government has many tools for macro-control, and analysts predict the government will strengthen efforts to ensure stable economic growth, especially investment growth, with the Belt and Road Initiative and the coordinated development of Beijing-Tianjin-Hebei region being highlighted.

Guan Qingyou, executive director of Minsheng Securities' research institute, said the political bureau meeting on April 30 indicates that the central leadership has noted the problem that the current fiscal policy is not proactive enough. Since the meeting emphasized increasing public spending, local governments may change their attitudes and increase investment in infrastructure.

He said most infrastructure investment will be made for regional revitalization, with focus on the Belt and Road Initiative, the coordinated development of Beijing-Tianjin-Hebei region and the Yangtze River economic belt. However, there should be some new ideas. For instance, the government could pay more attention to information infrastructure investment, and rely more on private investment such as public-private partnership.

Zhu Jianfang, chief economist of CITIC Securities Co. Ltd., said that in the short term, economic growth will still mainly rely on investment, while infrastructure investment is crucial to ensure stable investment growth. Although anemic demand will restrict investment growth, there are some active signals in the investment sector: The number of newly started infrastructure projects has rebounded; railway, power and pipeline network construction will shortly be accelerated to implement the Belt and Road Initiative; real estate sales have resumed growth after bottoming out, and real estate investment does not look set to drop sharply.

While several experts make their forecasts, their eyes--as well as the public's--will remain fixed on the Chinese economy to see how accurate their predictions turn out to be.

Copyedited by Kylee McIntyre

Comments to wangjun@bjreview.com