|

An end in sight?

How will this round of the currency dispute wrap up? Zhang Ming, an international finance expert at the Chinese Academy of Social Sciences, pointed out three possibilities.

First, the governments of all countries could reach a new Plaza Accords—an agreement reached by developed nations in 1985 to intervene in currency market—with the Chinese Government agreeing to appreciate its currency substantially in the next few years. Second, the Chinese Government could completely refuse currency readjustment, resulting in a trade war with the United States. Third, after international negotiation, the Chinese Government could agree to increase the flexibility of the exchange rate regime, but maintain control over the pace of the yuan appreciation.

Without a doubt, China's interests would be damaged by the first scenario. The second scenario will make both countries sink together. The third is the best, and most difficult, option but requires wisdom and candid cooperation from all leaders and countries.

But no one can argue a currency war is the last thing politicians want. At the G20 financial ministers and central bank governors' meeting held in South Korea on October 21-23, a joint communiqué was released, saying they would move toward more market-determined exchange rate systems that reflect underlying economic fundamentals and refrain from competitive devaluation of currencies.

The joint communiqué also noted their commitment to taking action at the national and international level to raise standards, so that national authorities implement global standards consistently, in a way ensuring a level playing field and avoiding fragmentation of markets, protectionism and regulatory arbitrage.

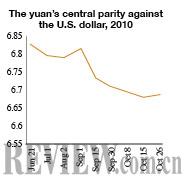

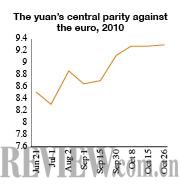

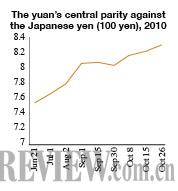

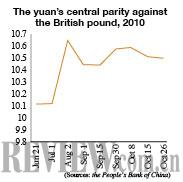

The currency disputes have highlighted the predicament the global currency system is facing: the dollar, a sovereign currency of the United States, also serves as an international reserve currency. The two functions are actually contradictory. If the U.S. Fed starts to print more money to spur its economic development, a dollar flood will sweep the world, causing huge damage to international financial stability. Therefore, it's time to establish a new monetary system, said Cao Yuanzheng, chief economist at BOC International (China) Ltd.

"The current global reserve currency is still the U.S. dollar. But its fluctuation has led to volatility in other currencies. A new international monetary system must be built or the existing one will collapse for good. Major economies should collaborate on this front to rebuild the international economic and monetary order," said Cao.

Developed countries' low interest policies

United States: In the first half of this year, the U.S. Federal Reserve withdrew part of its stimulus measures. But confronted with a recovery slowdown and impotent fiscal stimuli, the Fed started a new round. In July, it announced buying U.S. Treasury securities; in August, it ordered a cut to the excess reserve requirement ratio. A report issued by the Board of Governors of the Federal Reserve System on October 12 said the United States will keep the interest rates low and might start the second round of quantitative easing monetary policy, which means the Fed buys treasury securities and institutional bonds to inject liquidity into the market, to spur an economic revival.

Japan: The Bank of Japan, the country's central bank, slashed its benchmark interest rate from 0.1 percent to 0.1-0 percent to hold back the yen's appreciation. It is the third time for Japan to have a zero interest rate after 1999-2001. At the same time, Japan's central bank pledged to build a temporary fund of up to $60 billion to buy government bonds which is similar to the U.S. quantitative easing monetary policy.

Europe: The Bank of England decided to keep its key interest rate at 0.5 percent—the lowest level in history. The European Central Bank announced it would keep the key interest rate at 1 percent—also the lowest in history.

Australia: On October 7, contrary to most economists' forecast of an interest rate hike of 25 basis points, the Australian central bank announced to keep the current 4.5 percent rate to offset the Australian dollar's fast and passive appreciation against the U.S. dollar.

|