In 2006, Wal-Mart and Citibank were victorious in making Chinese acquisitions. Wal-Mart purchased Trust Mart, the chain store with the 11th largest sales volume in China in early 2006. Citibank won the ability to control Guangdong Development Bank, the third most profitable small and medium-sized commercial bank in China.

While transnational mergers and acquisitions have become a way to get more than a foothold in China, their spread indicates that China's market opening in 2006 was indeed broad.

Still regulating

Under China's WTO commitments, the transitional period ended on December 11, 2006. But even before this deadline, many industries had entered into the stage of free competition.

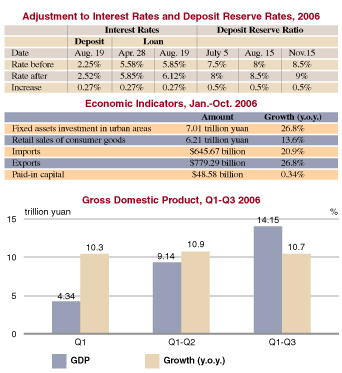

At the beginning of 2006, the Chinese Government, in order to make rational and effective use of foreign capital, drew up regulations on real estate and other sectors leaning toward monopolies or causing environmental pollution. Deemed restrictive by foreign companies, these policies caused some to worry that foreign investment would decrease, and this worry became the reality for some time. According to statistics from the Ministry of Commerce, from January to September, for instance, paid-in capital totaled $42.59 billion, dropping 1.52 percent compared with the same period last year.

However, foreign companies' favorable stance toward the Chinese market changed this trend in October. During that month, paid-in capital increased 15.92 percent year on year to $5.99 billion, raising the growth rate of the aggregate paid-in capital in the first 10 months to 0.34 percent over the year-earlier period.

At the same time, in 2006, China made a significant adjustment to its trade strategies. It rectified its tax rebate policy, reducing or even abolishing tax rebates on export products with high energy consumption and high pollution but low added value, while increasing rebate rates to exporters of hi-tech products. Further, it adjusted export and import tariff rates, increasing export tariff rates on resources and products of high-energy consumption and high pollution, but reducing import tariff rates on resources and products of science and technology. Changes in tax rebates and tariff rates restrained the impetus of products with low added value but enlarged imports of hi-tech products.

China's fulfillment of its WTO commitments related to reducing the overall tariff level allows abundant inflows of international commodities into China. The country's imports are catching up with its exports, and more and more international commodities are consumed in the Chinese market. This is good news to the world economy, since expanded Chinese consumption of foreign commodities can stimulate the growth of the world economy.

Hot, stable growth

"The Chinese national economy has kept a steady and rapid growth," said the Development Research Center (DRC) of the State Council in a research report on the Chinese economy released in November. The DRC research focuses on development trends in the Chinese economy.

But this stability is rooted in the strengthening of macroeconomic control measures adopted by the Chinese Government. In late 2005, China implemented a series of control measures, which have achieved some effects. But just when observers expected stable economic cooling in 2006, the economic performance in early 2006 made them wonder whether the economy was overheated. In the first quarter alone, fixed assets investment in urban areas surged 29.8 percent over a year ago, which was 4.5 percentage points higher than the rate in the same period last year. Newly increased loans were as high as 1.26 trillion yuan, accomplishing 50.3 percent of the amount for the whole year. The fast growth of fixed assets investment and newly increased loans led to overheating tendencies. Under these circumstances, the Chinese Government has to strengthen its macroeconomic control measures.

To cope with rapid credit growth, the government adopted a tight monetary policy, and has raised interest rates and deposit reserve ratio for commercial banks for three times since April.

Since the real estate sector is a major force driving investment growth, the State Council issued six measures on May 17 related to readjusting house supply structures and speeding up the formation of the low-rent housing system in urban areas.

In its Asian Development Outlook 2006 released in Beijing, the Asian Development Bank predicts that China's economic growth for 2006 will stand at 10.4 percent.

In its macroeconomic analysis and forecast report released on November 25, the Institute of Economics of Renmin University of China suggests that the Chinese economy faces a period of decline after rapid growth, but in 2006 China will still reach its highest GDP level in recent years, with the growth rate hitting 10.48 percent. According to the report, fixed assets investment in the year will shoot up 27 percent and the consumer price index will rise by 1.5 percent. Growth rates of narrow money and broad money supply will stand at 14.9 percent and 17.2 percent, respectively, while those of imports and exports will reach 27.2 percent and 23.4 percent, respectively.

Irrational structure

However, a review of the Chinese economy in 2006 shows that an irrational economic growth structure still impedes economic development. Li Daokui, Director of the Center for China in the World Economy of Tsinghua University, holds that in the present Chinese economic growth structure, ultimate consumption, investment and exports account for 55 percent, 40 percent and 5 percent, respectively, and the proportion of investment is still increasing. This structure is quite irrational, containing big risks. It is worrisome whether such a high investment proportion could be transferred into profitable projects in the future.

Yin Xiangshuo, professor at the Institute of World Economy of Fudan University, believes that the Chinese economy may not be overheated as a whole, but the structure is not reasonable. For example, too much capital is put into sectors like real estate.

As a result, overcapacity is seen in some sectors, which began in 2003 and remains unsolved.

According to Zhu Hongren, Deputy Director of the Bureau of Economic Operations of the National Development and Reform Commission (NDRC), in 2005, structural adjustment was made in some industries with serious overcapacity, and progress was achieved after that. But in the first half of 2006, investment was still expanding rapidly. The investment scope in some industries with overcapacity was enlarging and the number of newly begun projects was increasing at a high speed, bringing trouble that cannot be neglected.

Statistics of fixed assets investment projects above 5 million yuan indicate that among industries with overcapacity, only a few saw their investments decline and most others are still experiencing strong investment impulses. Their investment growth rates are far higher than the overall growth of fixed assets investment in urban areas.

Figures from the NDRC and the National Bureau of Statistics indicate that production capacity of the auto industry has been 3 million units more than the actual demand; the surplus capacity rate in the coking industry will reach 24 percent this year; in 2006, the production capacity of the cement industry will exceed 1.35 billion tons while the demand only stands at 1.05 billion tons; surplus capacity of the coal industry is 150-200 million tons; and in the iron and steel industry, the production capacity had reached 470 million tons by the end of 2005 although the estimated demand was only 300 million tons.

"Coping with overcapacity, we are facing severe challenges," said Zhu.

Beyond the irrational economic structure, there is another uncertain factor-the foreign exchange reserves of China have exceeded $1 trillion, making the country the largest foreign exchange reserve owner in the world.

What influence will such a large amount of foreign exchange reserves bring to the Chinese economy?

The economic circles both at home and abroad are still debating this issue.

|