|

Economic policies

China's favorable growth outlook warrants further normalization of the macroeconomic stance. After the large stimulus, the key macroeconomic concerns remain asset price increases, strained local government finances, and non-performing loans. While the inflation outlook does not seem worrisome, the upward risks call for vigilance and managing inflation expectations. Notwithstanding the slack and unemployment in many HICs, China's economy is operating close to full capacity and the growth outlook is favorable. Thus, further consolidation of the overall macroeconomic stance is needed to contain these risks.

Two-way risks to growth make it important to be able to respond flexibly to changes in circumstances. This can be done by ensuring flexibility in the design and implementation of policymaking. Over time, changes to the monetary and exchange rate regime to increase the leeway to use monetary policy to pursue domestic objectives, would help to deal with the divergence in the cyclical position vis a vis the United States and financial capital inflows amidst ample international liquidity.

The preparations for the 12th Five-Year Plan (2011-15) call for focus on structural issues and reforms. After the Fifth Session of the 17th Communist Party of China Central Committee (CPCCC) in mid-October, the CPCCC issued its proposal on formulating the 12th Five-Year Plan. This sets out the broad direction for policy making in the coming years. The major targets proposed include stable and relatively fast economic growth, major economic restructuring, raising people's income relatively fast, and deepening reform and opening up. The principles, targets, and tasks and strategic priorities are broadly in line with the overall challenges and objectives we discussed in our March 2010 China Quarterly (pp19-22) (Box 2).

|

Box 2. The Key Challenges and Objectives During the 12th Five-Year Plan1/

Two overall challenges:

- Achieving sustained rapid growth and development; and

- Improving the quality of growth, making growth more people oriented, improving the quality of life; reducing environmental degradation; containing energy demand; and reducing the external imbalance.

Five main objectives:

- Changing the economic growth pattern; more focus on services and consumption and less on industry and investment;

- Boosting efficiency, notably by innovation and upgrading and increasing the role of the private sector;

- Pursuing sustainable spatial transformation, by successful urbanization and regional development;

- Changing the role of the state in the economy, with less direct control when markets function well and more involvement in areas such as health and education where markets often do not function well; and

- Taking account of China's changing interaction with the rest of the world.

1/ For a discussion, see our March 2010 Quarterly Update (pp. 19-22). |

The Plan itself should have more specifics on the planned policy reforms and associated quantitative targets. In the June 2010 Quarterly we looked at the key role of the public finances and the crucial need for reform of the intergovernmental fiscal system, and fiscal reforms are likely to be introduced. Below we discuss two important policy areas in more detail: private sector development and energy.

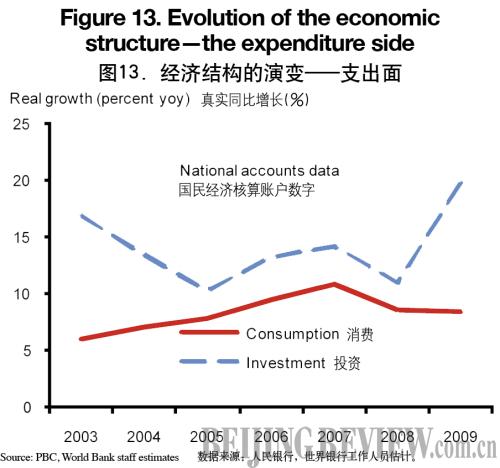

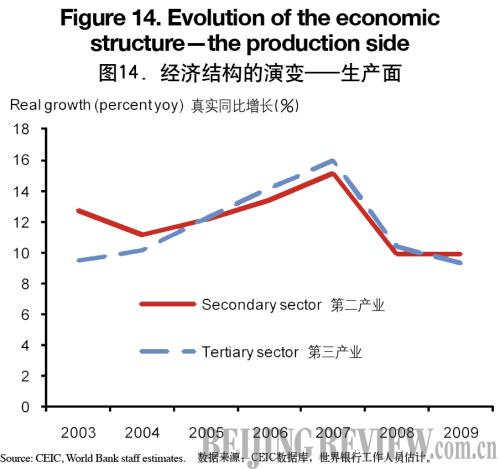

Key among the objectives is changing the growth pattern. This adjustment—toward more services and consumption, away from the emphasis on industry and investment—is in order to address China's social, environmental and external imbalances. It was already a key objective of the 11th Five-Year Plan. Progress has been made in several specific areas. However, there has been limited progress with the overall rebalancing. On the expenditure side, consumption has so far substantially lagged investment (Figure 13). On the production side, the tertiary sector has broadly kept pace with the secondary (largely industrial) sector but not grown faster, in real terms (Figure 14).

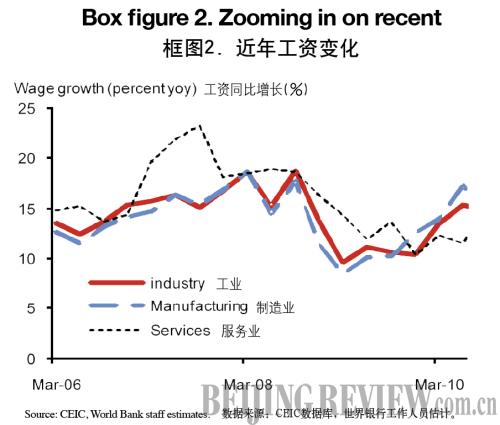

The need to transform the economic growth pattern may be stronger now than five years ago. This is in part because the external dimension has become more pronounced. Prospects for exports are less good now. Moreover, China's economy, its role in the world economy, and its external surplus are now substantially larger than five years ago. On current trends and policies, the current account surplus is rising again. Some have suggested that "endogenous" rebalancing may occur: Surplus labor is drying up and, thus, wage increases will be substantially higher in the years ahead, automatically driving up the share of wages and household income and thus raising the share of consumption and reducing the external surplus. However, in our view, the drying up of surplus labor is a slow process with still a long way to go. In any case, there are still various distortions in China's policy setting that need to be addressed, including in the prices of capital, labor and resources, as well as access to markets and finance. Removing the distortions is a key part of the required policy adjustment. Thus, in our view rebalancing to more domestic demand led, service sector oriented growth is unlikely without significant policy adjustment and it is appropriate to have it as a major objective of the 12th Five-Year Plan.

|