|

"Investing in Chinese companies equates to investing in China's future," said Senior Vice President of New York-based Guerrilla Capital Management Pang Ruifeng to China Business News. "Investing in Chinese companies equates to investing in China's future," said Senior Vice President of New York-based Guerrilla Capital Management Pang Ruifeng to China Business News.

China, as one of the world's largest economies, ensures very bright investment prospects, and U.S. stock investors have seen successful examples. Baidu's stock price soaring more than 10 times since its 2005 Nasdaq listing would partly explain Youku's first-day price surge, Pang said.

Chinese stocks are also irresistible because Chinese companies generally enjoy much higher growth potential and boast higher profit rates compared with U.S. companies, he said.

Not every IPO was a winner. Sky-Mobi and Bona claimed the worst and second-worst debuts, and lost 25 percent and 22 percent, respectively, on their first days last December.

True to its name

Carrying the labels of China's equivalents to YouTube, Amazon, Paramount and Apple Store, Youku, Dangdang, Bona and Sky-Mobi stirred investors' imaginations for lucrative returns in the future. But the SEC's probe reminded them that some of these IPOs might not be true to their names.

Compared with the domestic stock market, the NYSE and Nasdaq don't require the listing candidates to have a profit record for several consecutive years, and their requirements on profitability are replaceable if candidates can meet other requirements, which make U.S. IPOs a better choice for companies with great growth potential but in urgent need of funds to spur growth, said Fang.

About seven of the 41 Chinese companies listed in the United States last year posted negative net profits in 2009, he said.

Youku, for instance, currently reports a monthly loss of $2.7 million, compared with its monthly revenue of only $4 million.

But in contrast to China's stock markets in Shanghai and Shenzhen, American bourses have much stricter requirements for accounting accuracy and transparency. "This is what Chinese companies rushing to the U.S. stock market have to deal with in order to survive," he said.

U.S. investors have accused more than 20 Chinese companies of accounting fraud. Most recently, China's online apparel retailer Mecox Lane Ltd., which was listed on the Nasdaq in late October 2010, faced three class action litigations for inaccurate and misleading information in its IPO registration statement. This has led to its stock falling below the issue price.

In the same month, RINO International, a Dalian-based maker of environmental products, withdrew from trading on the Nasdaq after admitting accounting flaws.

"About 10-20 percent of Chinese companies are involved in accounting violations, but we still see that more than 80 percent of them live up to the standards of U.S. stock markets," he said.

It will also make them less trustworthy during the auditing if Chinese companies hired small accounting companies in order to seek a U.S. listing, he said.

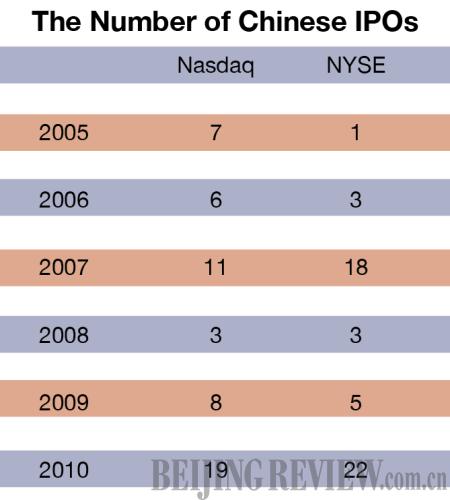

China has been Nasdaq's largest overseas market for three years, almost doubling the second largest in size, said Robert Greifeld, CEO of Nasdaq OMX Group in a China Securities Journal report.

In addition to the 19 IPOs, there were 24 over-the-counter bulletin board (OTCBB) updates or switches last year, making it a total of 166 Chinese companies listed on the Nasdaq by the end of 2010, according to Nasdaq statistics.

Very few OTCBB stocks, which were usually listed on the market through the "reverse takeover," are successful in making the jump from the market to the Nasdaq or any other major exchange. They are considered very risky and unstable because the OTCBB's listing requirements aren't as strict as the Nasdaq's or other major exchanges. |