|

2006, investor confidence has been encouraged and helped contribute to the most bullish stock market ever.

At the end of this September, the benchmark Shanghai Composite Index surged to 5552.3 points, doubling the final 2006 figure.

The Chinese stock market had been associated with policy, and most people referred to the mainland stock market as a "policy-directed market." The government was severely criticized by the public after the Ministry of Treasure tripled the stock stamp tax from 0.1 percent to 0.3 percent on the night of May 30, causing three days of consecutive stock price plunges and a sluggish June and July market. The harsh public criticism forced the government to turn to other solutions.

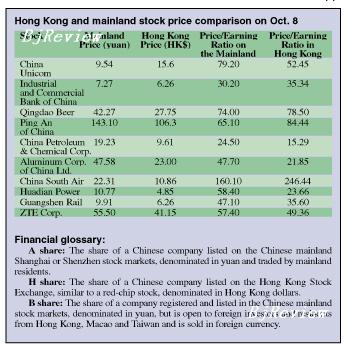

On September 20, the price/earning ratios of companies listed on the Shanghai and Shenzhen stock markets reached 62 and 70, indicating that the mainland market was the most expensive in the world. Again, the alarm bells rang around the government hallways.

"The 17th Congress of the Communist Party of China was going to be held very soon, and the authorities wanted the market to remain stable," said Huang Zefeng, strategy analyst with Haitong Securities. "There are three ways to cool the market: strengthening supervision to avoid manipulative trading, raising the interest rate and the reserve requirement rate, and expanding stock supplies."

The first two options did not seem to produce effective results. The authorities have continuously warned of illegal stock trading and punished those involved in stock market manipulation. At the same time, the central bank has raised the interest rate and reserve requirement rate five and seven times respectively so far this year, each rise followed by stronger stock price surge.

A source from the CSRC admitted to China Securities News that in order to resolve the liquidity problem, the key is to adjust the supply, not just the demand. The measures directed at killing investors' demand could not solve the problem, while providing good quality company shares is an effective way to achieve the sustainable development of the capital market.

The change of management methodology was thought-provoking for many.

Sun Bolei, a securities analyst, contended that the authorities had reached a consensus that the best way was to launch more IPOs to cope with the excessive liquidity.

This September alone, the authorities quickened the speed of IPOs. Altogether 13 new shares began to trade in the A-share market, raising nearly 150 billion yuan.

The fastest return came from the Construction Bank of China. It applied for listing on August 27, started its roadshow on September 11, and began to trade on September 25, just less than a month after application.

"This demonstrated the authorities' way of monitoring the stock market has changed," said Zheng Xiaofeng with Yingda Securities Co. Ltd.

Faced with the huge capital, the only thing to do now is to carry out IPOs of big companies to absorb the liquidity, according to Zheng. Currently, the number of good quality and big domestic companies not listed has shrunk, and the overall listing mode of listed companies may trigger stock trade manipulation. Therefore, the burden lies on the well-performed overseas listed Chinese companies.

Pan Feng, analyst with the research center of Galaxy Securities, said the larger the stock market is and the more big blue chips there are, the less stock manipulation of the stock market will occur. In order to pave the way for the launch of stock index futures, Pan believes it is paramount to further expand the stock market scale and introduce more large-scale blue chips into the maturing Chinese stock market. |