|

| Business |

| Managing Risks | |

| Financial asset management to be subject to uniform and practical regulation | |

|

|

|

Customers receive advice at the wealth management service counter of a bank in Shanghai (XINHUA)

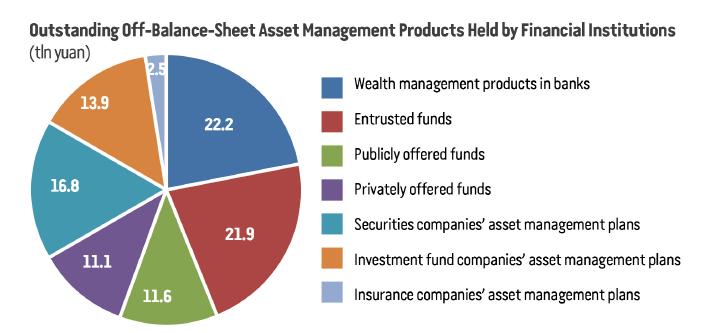

After five months of discussions and the soliciting of public opinion, China's central authorities issued a new guideline on asset management products and services on April 27, aiming to ensure the stability of the financial market and prevent financial risks with tightened regulation targeting the elimination of regulatory arbitrage in the sector. Uniform regulation Asset management business among Chinese financial institutions has grown rapidly in recent years. According to figures from the People's Bank of China (PBC), by the end of 2017, the outstanding off-balance-sheet asset management products held by all financial institutions had totaled 100 trillion yuan ($15.75 trillion). Among them, 22.2 trillion yuan ($3.5 trillion) of funds were off-balance-sheet wealth management products in banks; 21.9 trillion yuan ($3.45 trillion) were entrusted funds managed by trust companies; publicly offered funds and privately offered funds accounted for 11.6 trillion yuan ($6.3 trillion) and 11.1 trillion yuan ($1.75 trillion), respectively; while the asset management plans of securities companies, investment fund companies and their subsidiaries as well as insurance companies totaled 16.8 trillion yuan ($2.65 trillion), 13.9 trillion yuan ($2.19 trillion) and 2.5 trillion yuan ($393.7 billion), respectively. "Regulatory arbitrage activities are common because of inconsistent regulation rules and standards for similar kinds of asset management businesses, causing multi-layer investment, unclear risk limits, and potential liquidity risks in capital pools, wide spread implicit repayment guarantees and other problems. It actually led to a shadow banking system with insufficient regulation outside the official financial system," said a press release from the PBC. These problems have interrupted macro control, increased social financing costs, affected the quality and efficiency of the financial sector to serve the real economy, and exacerbated the transfer of risks from the financial sector to other industries and markets, said the PBC. To address these problems, the new guideline adopts classified regulation on different types of products and applies uniform regulation to the same type of products. The plan divides asset management products into publicly offered products and privately offered products on fund sources. For the use of capital, asset management products are divided into fixed income products, equity products, commodities, financial derivative products and mixed products. All asset management products must be clearly classified when issued, with the goal of selling suitable products to suitable investors. In addition, the guideline bans managing fund pools and requires independent management, booking and accounting of asset management products. Financial institutions will be required to improve product duration management, with the minimum maturity of closed-end asset management products set at no less than 90 days. This aims to restrict a short-termist business orientation, correct maturity mismatches between assets and liabilities, and prevent risks.

Market reactions The new guideline bans implicit repayment guarantees and adopts a net asset value approach. For individual customers, commercial banks will no longer be allowed to provide principal-protected or returns-promised wealth management products in the wake of the new regulation. With the net asset value approach, individual investors will get a better understanding of the risks and possible returns on their investment. "This will be positive to the sound development of the banking industry because the market and its participants will be more mature," said Zhu Yongli, General Manager of the Asset Management Department of China Zheshang Bank Co. Ltd. According to Pan Xiangdong, chief economist at New Times Securities Co. Ltd., since implicit repayment guarantees are banned, part of the funds previously allocated to wealth management products by commercial banks will flow to traditional deposit business, leading to banks losing interest in developing wealth management business. Zhao Yarui, senior researcher with the Financial Research Center at Bank of Communications, previously commented that a large amount of funds from asset management products were flowing to the stock market through multi-layered investment, but the new guideline will squeeze such funds out of the stock market. In the short term, capital inflows to the stock market may decrease, but the guideline will ultimately be conducive to long-term sound development as the market becomes well regulated, Zhao forecasted. Pan said the bond market may face the temporary pressure of decline due to lower capital inflow. "In the long term, however, since the guideline mainly targets the elimination of non-standard financing, the demand for standard assets, including certain types of bond products, will increase as regulation tightens. Therefore, development of the bond market still depends on the trend of the overall economy," Pan said. Xu Chengyuan, chief analyst at the Golden Credit Rating International Co. Ltd., noted that insurance asset management institutions are likely to gain more market shares of asset management as the guideline establishes a fair competition environment. According to him, insurance asset management business has always been subject to strict risk control and moderate investment preferences because the safety of funds is the top priority of such companies. "Since they are already subject to very strict regulation, these institutions will be less affected by the guideline than other types of asset management institutions," said Xu. You Yu, Executive Vice President of Zhongrong International Trust Co. Ltd., said the financial market is not expected to be significantly affected. "Compared with the draft version, the final version of the guideline makes some adjustments regarding market conditions that make it more practical and professional," he said. In addition, the final version also includes changes beyond market expectations. For example, the transition period was extended to 2020, which allows more time for market participants and the regulatory authorities to react. "This is more practical and will alleviate market fluctuations," said You. Copyedited by Rebeca Toledo Comments to wangjun@bjreview.com

|

|

||||||||||||||||||||||||||||||

|