|

| Business |

| Looking for the Next Great Company | |

| Private equity needs to find better exits and overcome other hurdles for higher returns | |

|

|

|

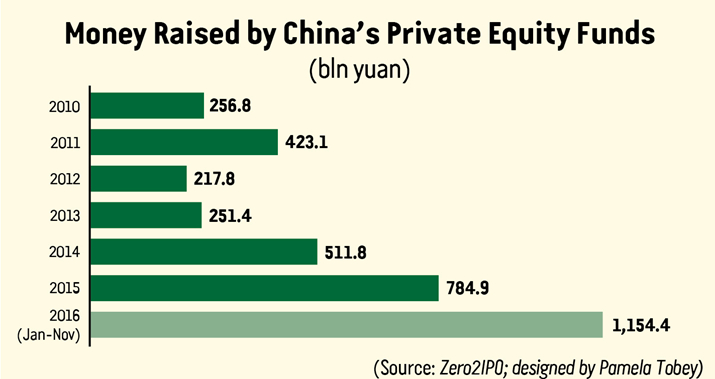

Panelists discuss the opportunities and challenges for China’s PE firms at the Eighth Global PE Beijing Forum held on December 10 (COURTESY OF BEIJING PRIVATE EQUITY ASSOCIATION) Hugo Shong has been founding general partner of IDG Capital Partners, a Chinese investment firm active in the technology sector, since 1993. He also has been founding general partner of the IDG-Accel China Growth Fund since 2005 and the IDG-Accel Capital Fund since 2008. A legendary private equity (PE) investor, Shong has invested in more than 500 Chinese companies, of which over 100 have been listed on the stock market or merged or acquired. But the investment that he is proudest of took him only two hours to decide. "Five years ago, I had a stopover in Los Angeles during which I visited a media company in Burbank called Legendary Pictures," Shong said on the sidelines of the Eighth Global PE Beijing Forum held on December 10, 2016. "The company had only 30 staff, but the box office receipts of the movies it produced were more than those of China's two largest state-owned film groups combined. It focused on the production of Hollywood blockbusters, a revenue model I found very interesting. After the visit, I decided to invest 85 million yuan ($12.26 million) in the company." To his delight, the films produced by Legendary Pictures, such as Inception, Pacific Rim and Jurassic World, became money-spinners around the world. In January 2016, Chinese conglomerate Dalian Wanda Group acquired the company for $3.5 billion in cash, marking China's largest cross-border cultural acquisition to date. The deal helped Shong get more returns on his investment than he could have imagined. According to data from Zero2IPO, a provider of investment banking and financial advisory services, in the first 11 months of 2016, Chinese PE funds raised more than 1.15 trillion yuan ($166.58 billion) altogether, a huge jump from last year's 784.9 billion yuan ($113 billion). China is now the world's second largest PE market, after the United States. The size of the market expanded fifty-fold from 2006 to 2015. In the next three to five years, the sector is expected to grow exponentially, said Fu Xinghua, Vice President of Zero2IPO. "The number of active PE firms has exceeded 10,000, and new funds and new market entrants are growing in large numbers," Fu said. According to Huo Xuewen, Director General of the Beijing Municipal Bureau of Financial Work, PE investment is the best way to encourage the financial sector to support the development of the real economy. Once this channel is cleared, funds will be transported to the real economy. The blossoming of PE investment offers new hope to the country's economic rebalancing act. However, an underdeveloped regulatory system, a lack of exit routes and susceptibility to unpredictable policy changes are the major obstacles standing in the way of further growth.

Shao Bingren, Chairman of the China Association of Private Equity, delivers a speech at the opening ceremony of the Eighth Global PE Beijing Forum on December 10 (COURTESY OF BEIJING PRIVATE EQUITY ASSOCIATION) A booming market Shao Bingren, Chairman of the China Association of Private Equity, said PE investment is being recognized by more and more people as a wise way to increase their wealth. "State-owned capital has become a major force in supporting the development of the PE market in China, with more and more state-owned enterprises (SOEs) setting up PE funds to make investments. Predictably, the market won't fall short of money in years to come," Shao told the Beijing forum. However, Shao warned that the presence of state capital would, to a certain extent, squeeze the share of private capital in the PE market. He suggested state capital play a bigger role in government-supported sectors with large financing demands, while private capital, with more agility and more market-based operations, engage in sectors with more competition. The attendees of the forum had several tips for making wise investment decisions. "We take baby steps and constantly reflect on previous investment cases," said You Wenli, Managing Director of Beijing Shougang Fund. According to You, when investing in a startup, one should consider two aspects—the team, "whether it has worked together for long enough; whether team members complement each other and what their business performance is like," and the system, "whether the company has a suitable system." Liu Xing, partner at Sequoia Capital China, said the pace of making investments is of critical importance. "If you invest in too many companies, you have to manage those companies, and you'll have less time and energy to look for new opportunities," Liu warned. "[Also,] calmness is especially needed in times of asset bubbles." According to Veronica Wu, Co-President of the CSG Group, valuation of startups is more reasonable now than in 2014 and 2015, when there were a lot of asset bubbles. Therefore the profit margin has increased for PE funds. Industrial insiders believe new investment opportunities exist in sectors that can meet the demand for quality products and services, including higher-end healthcare, education, sports, culture and tourism. "The year 2017 will see a higher demand for professionally competent PE investors. It's not only about the money. Startups want investors who can best understand them to be their partners," Liu said. Finding the right exit Since April 2016, to curtail mounting financial risks, registration of finance-related businesses has been suspended in China, including investment management firms, PE funds, peer-to-peer lending platforms and online lending companies. "Some companies are engaged in illegal fundraising under the guise of PE investment. But that's not the fault of PE funds. Illegal fundraising existed even before PE investment was invented," Shao said. He suggested the regulatory authorities strengthen during and after establishment regulation instead of imposing new market entrance thresholds. "Right now, the regulatory authorities are using the supervisory mentality for securities on PE investment. That's completely wrong," Shao said. He also said the exit methods of PE funds should be broadened, with a better-regulated securities market and a multi-layer capital market. The lifecycle of every PE transaction has four stages: raising money from investors, investing in a company, managing the company and finally, exiting it. Several methods are used for investors to exit their investment—through initial public offering (IPO), sale of PE-owned assets to strategic buyers, transactions between PE buyers and sellers, and finally, leverage recapitalization. Though an IPO can get investors the highest return on investment, the listing of the shares of a company is subject to strict regulatory requirements, which makes the IPO a lengthy and expensive process. It is also susceptible to unpredictable policy changes. To curb equity market fraud, China's securities regulator, the China Securities Regulatory Commission (CSRC), suspended IPOs from November 2012 to January 2014. Then, in the face of a stock market rout, the CSRC did it again from July to November 2015 due to sharp market fluctuations. Since its inception in 1999, a lack of exit routes has plagued the Shenzhen Capital Group. Of the more than 600 companies it invested in, less than 200 were listed on the stock market. "Sudden policy changes regarding exit methods, IPO regulations in particular, have a huge impact on the PE industry. Sometimes we feel really pained," said Zhong Lian, Vice President of the Shenzhen Capital Group. John Gu, PE head at KPMG China, said the main reason behind frequent government intervention is that the stock market is full of individual investors and short of institutional investors. "Therefore, a stock market rout will severely affect people's livelihoods and the government has to do something," Gu said. "Institutional and long-term investors should be developed." Cheng Jiuyan, General Manager of Beijing Equity Trading Center Co., said pinning all hopes on IPOs is unrealistic. "IPOs shouldn't be the only hope for PE funds to exit their investments. If you focus only on IPOs, you will face a grim prospect, because very few of those startups could get listed eventually," Cheng told Beijing Review, adding it's time for China to develop new equity transfer schemes. China's capital market has several layers. The first consists of the main boards of the Shanghai and Shenzhen bourses; the second is a board for small and medium-sized enterprises at the Shenzhen bourse; the third is the National Equities Exchange and Quotations system; and the fourth refers to regional over-the-counter markets for equity transfers. "The third layer and the fourth layer, which is being piloted by individual cities, could be a perfect exit channel for PE funds. Securities brokers for these markets should be cultivated to enhance trust between buyers and sellers," Cheng said. Copyedited by Sudeshna Sarkar Comments to zhouxiaoyan@bjreview.com |

|

||||||||||||||||||||||||||||

|